Why the Rupee Is Weakening: Oil Prices and Geopolitical Risks Explained

When headlines say the rupee has hit an eight-week low, the impact is not limited to currency traders. A weaker rupee can affect fuel bills, grocery costs, travel budgets, education expenses, loan decisions, and investment returns. For Indian households, the key issue is how quickly global shocks move into everyday financial planning.

The rupee has come under pressure as crude oil prices surged above USD 105 per barrel and U.S.-Iran tensions added fresh fear to global markets. Reports such as Indian Rupee Hits Historic Low Amid Rising Oil Prices and US-Iran Tensions and Reuters coverage on the rupee’s rough patch point to oil prices, foreign outflows, and geopolitical uncertainty as major pressure points. The situation matters because India depends heavily on imported crude, so higher oil prices increase the need for dollars and can weigh on the rupee.

US-Iran tensions have made energy markets nervous because the region is important for oil supply and shipping routes. When investors see higher geopolitical risk, they often reduce exposure to emerging markets and move toward assets they view as safer. This can affect foreign portfolio investor flows, equity market sentiment, commodity prices, and the broader mood across the NSE and BSE.

Link Between Global Crude Prices and India’s Import Bill

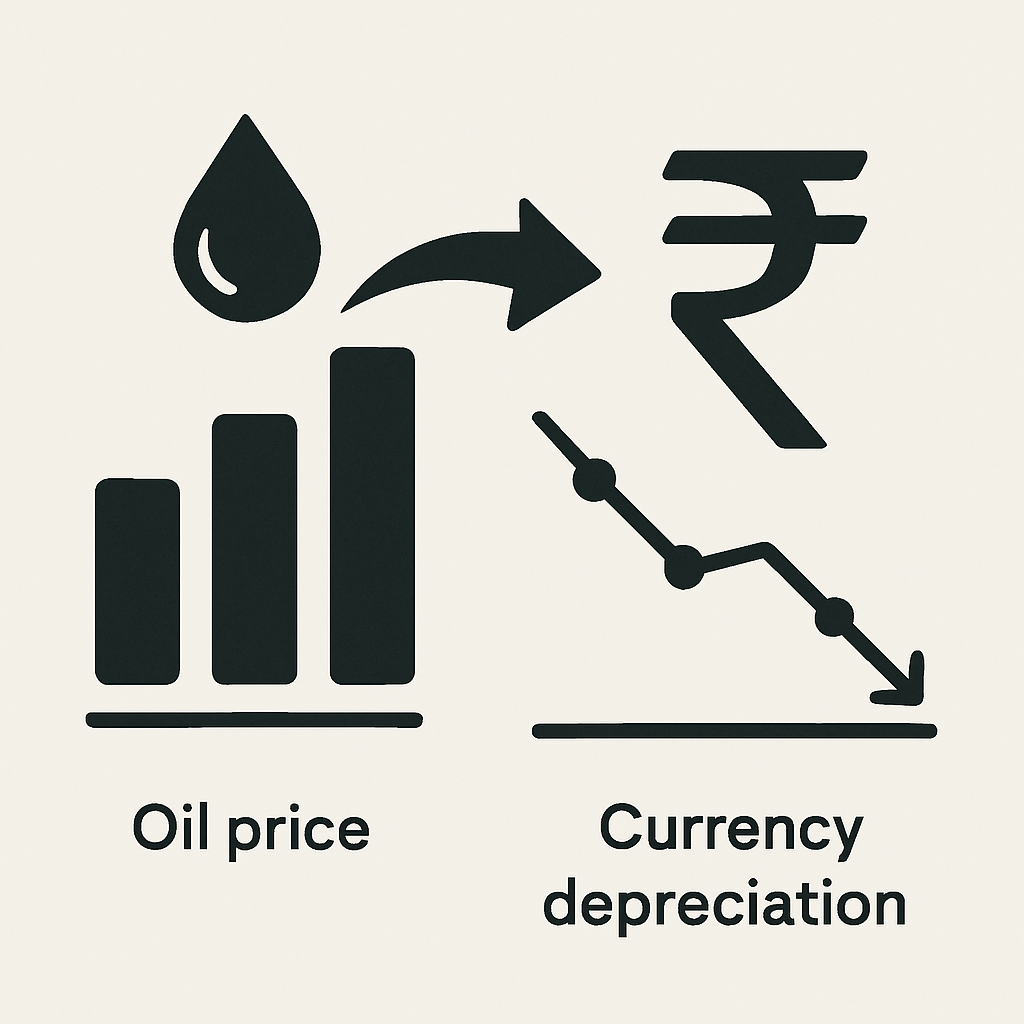

Higher crude prices affect the rupee through India’s import bill. When oil becomes costlier, refiners and importers need more foreign exchange to pay suppliers, which raises dollar demand. If dollar demand rises faster than inflows, the rupee can face depreciation pressure.

A research paper on the impact of crude oil prices on the Indian rupee explains this balance of payments channel. Rising oil prices can widen the current account deficit, increase demand for foreign exchange, and put pressure on the domestic currency. The same chain can also raise inflation through fuel, freight, and production costs.

This is why an oil shock can quickly become a household finance issue. Fuel prices affect transport, and transport affects the movement of food, raw materials, and finished goods. Even families that do not drive daily can feel the impact through groceries, delivery fees, school transport, and utility costs.

Geopolitical Tensions: Impact Beyond Oil

Geopolitical stress does not affect only crude oil. It can also hurt investor confidence and increase volatility in currency, equity, and commodity markets. When global funds reduce risk, money may move away from Indian equities and debt, which can add pressure on both markets and the rupee.

Foreign portfolio investor flows are important because they influence market liquidity and sentiment. If outflows continue during an oil-price spike, the rupee may face more pressure and stocks may remain choppy. You can read more on this theme in PocketPlanGuru’s guide on why foreign investors withdraw billions and what it means.

Investors should avoid reacting to every headline as if it will become a long-term crisis. Geopolitical events can escalate, ease, or remain unresolved for weeks. A calm review of risks is more useful than panic buying, panic selling, or chasing short-term market calls.

Role of RBI in Currency Stability

The Reserve Bank of India closely tracks rupee volatility, inflation, and foreign exchange market conditions. It may use foreign exchange reserves to reduce sharp currency swings when markets become disorderly. Such action can calm panic, but it cannot directly control global crude oil prices or geopolitical outcomes.

The RBI can also use monetary policy tools when inflation pressure rises. Repo rate decisions affect home loan EMIs, personal loan rates, fixed deposit returns, and debt fund performance. Investors should follow official updates from the Reserve Bank of India instead of relying only on market rumours or social media predictions.

Currency intervention and interest rate decisions have limits, so households should not build financial plans around one policy move. A weaker rupee may last longer than expected if oil prices stay high or foreign outflows continue. A stronger rupee can also return if crude cools, inflows improve, or global risk appetite recovers.

How the Rupee Slide Affects Household Budgets in India

When the rupee weakens, imports become costlier in rupee terms. Crude oil is the most visible example because it affects petrol, diesel, transport, logistics, and several production chains. Over time, these higher costs can appear in household budgets across large cities, small towns, and semi-urban areas.

The impact will not be the same for every family. A household with a long daily commute may feel fuel costs faster, while a family that spends more on groceries may notice price changes through food and delivery bills. A family with rent, school fees, EMIs, medical costs, and insurance premiums may need a broader budget review.

The best first step is to separate essential spending from flexible spending. Essentials include rent, EMIs, groceries, utilities, insurance, school fees, and medical needs. Flexible spending includes subscriptions, dining out, impulse shopping, premium delivery services, and non-urgent travel.

Impact of Rising Fuel Prices on Daily Expenses

Petrol and diesel prices influence more than the cost of filling a vehicle. Higher diesel costs can raise transport charges for vegetables, grains, dairy, medicines, and packaged goods. That is why food inflation can rise even when a household’s own fuel use is limited.

Cooking fuel, electricity, and delivery charges may also become costlier over time. Businesses often pass higher logistics and input costs to customers when margins shrink. PocketPlanGuru has a detailed guide on what rising crude oil prices mean for your budget if you want a deeper household view.

Families should watch recurring expenses because small increases can add up quietly. A higher fuel bill, a higher grocery bill, and higher school transport charges may look manageable separately. Together, they can reduce monthly savings and force people to delay investments or emergency fund contributions.

Practical Budget Recalibration Steps

Start by tracking your spending for at least one full billing cycle. Split expenses into essentials, lifestyle spending, EMIs, insurance, investments, and irregular costs. This simple exercise shows where money is leaking without forcing emotional cuts to important goals.

Bulk buying may help for non-perishable essentials if prices are rising steadily and storage is practical. Public transport, carpooling, route planning, and fuel-efficient driving can reduce daily costs. Credit card rewards on fuel or groceries may help, but unpaid balances can wipe out the benefit through interest charges.

It is also useful to create a temporary inflation buffer in the monthly budget. This buffer can cover sudden increases in food, transport, utilities, and medical costs. If the buffer is not used, it can be moved to the emergency fund or a goal-based savings account.

Coping With Inflation on a Fixed Income

Retirees and fixed-income households need extra care during high inflation phases. A sudden rise in fuel, food, and healthcare costs can reduce purchasing power quickly. Keeping enough liquid money for medical bills, utility spikes, and sudden travel needs can reduce stress.

Long-term products such as PPF, NPS, EPF, and insurance-linked savings should not be broken without checking rules, penalties, liquidity limits, and tax impact. Some bank deposits may provide stability but may not beat inflation after tax. A financial advisor can help review whether the income plan still matches monthly needs and risk tolerance.

Fixed-income households should avoid taking large risks only to chase higher returns. Products that promise high returns may carry credit risk, liquidity risk, or market risk. Safety, predictability, and access to cash are often more important than squeezing out a small extra return.

Investment Strategies to Manage Currency and Inflation Risks

A rupee slide is a reminder to review portfolio risk, not a signal to make rushed decisions. Currency depreciation and inflation can reduce real returns even when portfolio values appear stable. A diversified portfolio can handle shocks better than a portfolio concentrated in one asset class or one theme.

This does not mean investors should blindly rush into gold, global funds, commodity funds, or sector funds. Each product carries its own risk, cost, tax treatment, and liquidity profile. Investors should consult a financial advisor before making product-specific changes.

The right response depends on age, income stability, goals, time horizon, and risk capacity. A young investor with a long SIP horizon may respond differently from a retiree who depends on monthly income. A business owner with dollar expenses or import exposure may need a different plan from a salaried investor with domestic expenses.

Fixed Income Options During Inflationary Periods

Some investors review government securities, high-quality fixed income products, short-duration debt funds, and bank deposits during inflationary periods. These products differ in interest rate risk, credit risk, taxation, liquidity, and return expectations. Product suitability should be checked with a financial advisor before investing.

Short-duration debt funds may face lower interest rate sensitivity than long-duration funds, but they are not risk-free. Bank fixed deposits can offer stability, though post-tax returns matter for investors in higher tax brackets. Section 80C products such as PPF and certain tax-saving deposits may support tax planning, but they also come with lock-ins and liquidity limits.

Debt allocation should not be selected only on the basis of headline yield. Investors should understand whether returns are fixed, market-linked, taxable, or subject to exit loads. If the goal is near-term safety, capital protection and liquidity may matter more than return maximisation.

Gold and Commodity Exposure as Traditional Hedges

Gold often attracts attention when the rupee weakens and geopolitical fear rises. Indian investors may access gold through physical gold, gold ETFs, or Sovereign Gold Bonds, depending on suitability and availability. These options differ in storage needs, liquidity, taxation, pricing, and holding-period rules.

Gold should not become the entire hedge for a household or portfolio. It can move sharply and may underperform for long periods. A financial advisor can help decide whether any gold allocation is suitable based on goals, time horizon, and existing assets.

Commodity-linked products can be volatile because prices react to global supply, demand, currency moves, and political risk. A short-term spike in oil or gold does not guarantee long-term gains for investors. Any exposure to commodities should be sized carefully and reviewed as part of the overall financial plan.

Equities and Mutual Funds With Domestic and Global Exposure

International mutual funds can provide exposure to foreign assets and may partly offset rupee weakness in some conditions. They also carry market risk, currency risk, taxation issues, expense ratios, and regulatory limits. Investors should consult a financial advisor and read fund documents before investing.

Domestic equities may show resilience through exporters, defensive businesses, and companies with pricing power. However, not every exporter benefits equally from a weaker rupee because input costs, hedging policies, competition, and global demand also matter. SIP investing can reduce timing stress, but it does not remove market risk.

For broader equity context, read PocketPlanGuru’s article on why proven midcap stocks matter for your portfolio. The same principle applies during currency volatility: quality, valuation, diversification, and suitability matter more than headlines. Investors should avoid shifting large sums into a theme only because it appears to benefit from a weaker rupee.

Sector Outlook: Possible Winners and Losers

A weaker rupee and higher oil prices do not affect all sectors equally. Some companies may gain from export income or higher commodity prices. Others may face higher input costs, weaker margins, or softer consumer demand.

Investors should avoid broad guesses and study business models carefully. Debt levels, margins, import dependence, pricing power, and currency hedging policies can change the outcome for each company. Sector indices on the NSE website can help track market trends, but they should not replace proper research.

Sector views should be treated as risk indicators, not as direct buy or sell instructions. A sector that appears strong can still contain weak companies, and a pressured sector can still contain resilient businesses. Investors should consult a financial advisor before making sector-specific allocations.

Sectors That May Show Relative Resilience

Export-oriented IT and pharmaceutical companies may benefit when dollar revenue converts into more rupees. Some businesses with foreign income and domestic costs may also see support from currency depreciation. However, global demand, client budgets, regulation, and hedging decisions can affect the final outcome.

Energy-related companies may benefit in some parts of their business when crude prices rise. The benefit is not automatic because pricing rules, refining margins, input costs, subsidies, and policy decisions can alter results. Investors should avoid assuming that every oil-linked company will gain from higher crude prices.

Defensive sectors may attract interest when markets turn volatile. These businesses often sell essential goods or services, which can make demand more stable. Even defensive stocks can become risky if valuations are stretched or earnings disappoint.

Sectors That May Face Pressure

Aviation often faces pressure when fuel costs rise because fuel is a major operating expense. Automobile companies may also feel pressure through higher input costs, weaker buyer sentiment, and financing costs. Import-heavy electronics, luxury goods, and some retail businesses may face pricing stress when the rupee weakens.

FMCG firms may struggle if consumers trade down to cheaper products. Companies with high debt can suffer more if borrowing costs stay elevated or cash flows weaken. Higher inflation can also affect discretionary spending on travel, gadgets, premium products, and entertainment.

These risks do not mean every company in these sectors will perform poorly. Strong brands, efficient cost structures, pricing power, and low debt can improve resilience. Investors should review company fundamentals and consult a financial advisor before acting on sector trends.

Portfolio Review Based on Sector Trends

Sector rotation can tempt investors during volatile markets. Concentrated bets can hurt if oil prices reverse, geopolitics improves suddenly, or market expectations change. Diversified equity funds, balanced advantage funds, and asset allocation funds may reduce single-sector dependence, but suitability varies by investor.

Check whether your portfolio already has enough exposure to energy, IT, pharma, banks, consumption, and global themes. Rebalancing should follow your financial plan rather than daily headlines. For stock or fund selection, consult a SEBI-registered investment advisor and review disclosures on the SEBI website.

A portfolio review should include emergency funds, insurance, loans, tax planning, and asset allocation. Investments do not operate separately from household cash flow. If inflation is hurting monthly savings, the portfolio plan may need adjustment even if market returns look acceptable.

Long-Term Geopolitical Risks and What They Mean for Indian Investors

The rupee’s eight-week low may be a short-term headline, but the risk behind it can last longer. U.S.-Iran tensions can keep energy markets nervous if supply fears continue. Global investors may also demand higher risk premiums from emerging markets during uncertain periods.

Research from ING on what lies ahead for the Indian rupee in a higher oil price environment highlights balance of payments stress and possible policy responses. India has managed external shocks before, but each cycle brings different challenges. Households and investors should prepare instead of panic.

The practical response is to build flexibility into both budgets and portfolios. A family with an emergency fund, adequate insurance, controlled debt, and diversified investments can handle volatility better. A family that depends on short-term borrowing or has no buffer may feel the pressure faster.

Potential Geopolitical Scenarios and Market Impact

If tensions escalate, oil prices may spike further and the rupee may face added pressure. This can increase inflation and keep equity markets volatile. In that situation, households may need tighter budgets and investors may prefer a more cautious review with a financial advisor.

If diplomacy improves, oil prices may soften and markets may breathe easier. Lower crude prices can reduce pressure on inflation and the trade deficit. The rupee may still depend on other factors, including foreign flows, interest rate expectations, and global risk appetite.

A long, uncertain middle path is also possible. Markets may remain volatile without a clear trend, and households may face gradual cost increases rather than one sudden shock. This is why periodic review is better than making one large decision based on a single headline.

Diversification and Risk Management

Diversification means spreading assets across Indian equities, fixed income, cash, gold, and suitable global exposure if appropriate. The goal is not to predict every currency move correctly. The goal is to reduce the damage that one shock can cause to the full portfolio.

Protection should not be ignored while chasing returns. Term insurance, health insurance, and an emergency fund protect families from forced selling during market stress. Tax planning through ITR filing, Section 80C, NPS, EPF, and PPF should support financial goals rather than drive every investment choice.

Debt management also matters when inflation rises. High-interest personal loans and credit card balances can become a bigger burden if monthly expenses increase. Reducing expensive debt may improve financial resilience more than chasing a short-term investment theme.

Staying Updated Without Overreacting

Follow RBI policy updates, crude oil trends, foreign portfolio investor flows, and SEBI announcements. Also watch repo rate changes because they affect loans, deposits, and debt funds. Major global events can change market mood quickly, so information should come from credible sources.

A quarterly portfolio review works well for many long-term investors during uncertain periods. A review may be needed sooner after a major policy move, sharp oil shock, or major geopolitical event. If you feel unsure, consult a financial advisor before making large changes.

Staying informed does not mean checking prices every hour. Too much noise can lead to emotional decisions and unnecessary trading. A written plan for savings, investments, insurance, and debt can keep decisions grounded when markets become volatile.

Frequently Asked Questions

How will rising oil prices affect my monthly expenses?

Higher oil prices can raise petrol, diesel, transport, and logistics costs. These costs may then show up in grocery bills, delivery charges, school transport, and daily commute expenses. Review your monthly budget, identify flexible spending, and keep a small inflation buffer where possible.

Can I protect my investments from rupee depreciation?

You can manage risk through diversification across suitable assets such as equities, fixed income, cash, gold, and global exposure where appropriate. No single product can fully protect a portfolio from currency depreciation, inflation, and market volatility at the same time. Consult a financial advisor before making product-specific investment changes.

Is the RBI expected to intervene to stabilise the rupee?

The RBI monitors currency volatility and may use foreign exchange reserves when markets become disorderly. It can also use policy tools to manage inflation pressures and support financial stability. These steps can reduce sharp moves, but they cannot control global oil prices or geopolitical developments.

Which sectors should Indian investors watch now?

Export-oriented IT, pharmaceuticals, energy-linked businesses, and defensive sectors may show relative resilience in some conditions. Aviation, autos, import-heavy businesses, and some discretionary consumption segments may face pressure from higher costs or weaker demand. Sector investing carries risk, so consult a financial advisor before making allocation decisions.

How often should I review my portfolio amid geopolitical tensions?

A quarterly review is a practical schedule for many long-term investors. Review sooner if oil prices spike sharply, the RBI changes policy, foreign outflows intensify, or global tensions escalate. Keep SIPs, emergency funds, insurance, and debt repayment aligned with your overall financial plan.

The rupee’s eight-week low shows how global events can quickly affect Indian wallets. Oil prices, inflation, RBI policy, and foreign flows can shape household budgets and investment returns in the months ahead. Stay informed, review your plan calmly, and subscribe to PocketPlanGuru for clear insights on protecting your wealth.

Disclaimer: The information above is for educational purposes only and does not constitute financial advice.